BY JAMES HUSSAINI April 13, 2015My last article covered the initial steps to starting your own real estate brokerage. Let’s continue with the next steps once you’ve created and registered your business, hired your staff and found your location. Day-to-day administration There are a lot of hassles in operating your own brokerage. Obviously, the more salespeople you have, the more paperwork involved. Some of the regular but crucial duties are: Transaction coordination With every deal that gets to your desk, you have to handle the details. You have to start with making sure that you have all required documents. In order not to scratch your head each time to remember, you should have a “Transaction Checklist.” With recent changes in regulations, having some of the documents is crucial. In addition to document collection, you have to coordinate constantly with the lawyers of both sides for closing the deal out. Fund disbursements “Trade Record Sheets” are instrumental in directing your fund disbursements. Once the deal is closed, it is time to disburse the funds through proper channels, such as bank accounts, to different sources, such as brokerages. Understanding the funds disbursement procedure is at the core of brokerage process. If you don’t have a proper process in place, you are taking the risk of jeopardizing your brokerage license with the Real Estate Council of Ontario (RECO). Accounts reconciliations Reconciling accounts is at the heart of RECO’s requirement for real estate brokerages. A broker of record is required to reconcile all accounts on a monthly basis. Of course, there are many other paperwork requirements, but account reconciliation is the most important one. It is a crucial task, but it is the most daunting. No one likes to do their monthly reconciliations. It is very time-consuming and needs a lot of patience. Brokers of record and managers are tempted to postpone this crucial and “boring” task. Accounts reconciliations are at the pinnacle of importance compared to all other details of all the accounts that you have to record and report. Your annual tax filings require accounting files, which is another topic in itself. Although there are many accounting software programs available, such as QuickBooks, that might make your life easier, all reports and reconciliations still need your involvement and signature. Filing and record-keeping Of course, a brokerage is required by both RECO and the Canada Revenue Agency (CRA) to keep records of all transactions. Brokerages are constantly referring to their paperwork long after closed transactions for many different reasons, not to mention RECO inspections, FINTRAC record requests and CRA audits. It is important to have a filing system in place at the time of inception of your brokerage; color-coding has been proven to be one of the most effective methods of organizing files. With the rapid developments in technology and online storage, not only are a lot of hassles taken care of, but also one can access their transaction documents from anywhere, anytime. Supervising staff Not only do you have to prepare plans and processes for your staff, but more importantly you have to make sure that you implement those processes. Planning is much easier compared to implementation, especially when it comes to your staff. You might have the best systems and online management software to handle all aspects of your brokerage, but it still needs your monitoring. No matter how reliable and trustworthy your staff is, you still need to be involved and engaged with them. Industry and regulatory changes Like any other industry, there are rules and regulations that govern the real estate industry. The rules are written in stone and still change, sometimes without notice. With recent rapid advancements in technology, the changes are more rapid than ever before. These changes can come from regulatory bodies within our industry or outside. Some of the organizations that can impact on your brokerage business are:

You have to keep yourself up-to-date with the changes in your regulatory environment. Not only do you have to be aware of changes to regulations and compliance issues, but you have to make the necessary changes within your systems and office processes to show that you are following the rules. Managing ongoing overhead and operating expenses Perhaps none of the above concerns compare to the stress of the risk of money coming out of your pocket each and every month whether you are generating revenue or not. You not only have to pay your office rent but also your payroll and many other regular miscellaneous expenses, such as phone systems, Internet, after-hours answering services, equipment rental, supplies, etc. The worry about ongoing expenses against cyclical revenues is usually the greatest concern that stops most brokers from opening their own real estate brokerage. Overcoming obstacles and implementing solutions Real estate brokers operate in a “risk versus reward” economy. There is no hourly wage, only upfront expenses and time spent with a cyclical paycheck based solely on completed deals. When you decide you are worthy of the challenge of brokerage ownership, after having examined and solved the obstacles as described above, it’s time to take your real estate career to the next level. The benefits of owning your brokerage, for the true entrepreneurs, outweigh the risks because the risk involved is minimal. One of the solutions of keeping your ongoing expenses manageable, and on budget, is based on the current trend of the “sharing economy” and is similar to “business center office services.” When you can hand over the majority of nonselling tasks to experienced and competent staff that you pay on a contingency or flat-fee basis, you can budget your expenses. This delegation allows you to always recognize your income potential with every deal that crosses your desk. This model not only takes care of tasks and details but also cuts down the cost of office setup, renovation, furnishings and even administrative staff. With recent disruptions in our industry, now it is possible to open and manage your own brokerage without the hassle. Read “A step-by-step guide to launching your own brokerage — Part 1” here. James Hussaini is the founder and president of Realty Point. Email James Hussaini. Read the article in INMAN

0 Comments

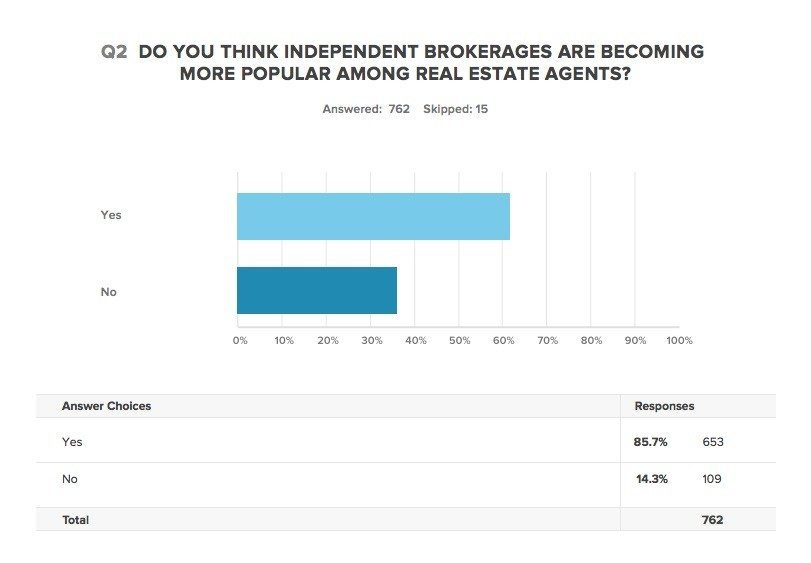

BY JAMES HUSSAINI April 03, 2015 Despite all its benefits, what discourages top-performing real estate brokers from owning their own real estate brokerage? In the same way that business ownership is not for everyone, brokerage ownership is not for every real estate agent. In addition to the desire to own a business, there are certain qualities that define a true entrepreneur. None of these qualities are as important as the internal courage to take calculated risks. If there is no risk at all, it will not be a lucrative business. A businessperson is a risk taker with a “type A” personality, with exceptional leadership skills and the ability to guide others past the concerns of the business risk. That risk must be tempered with vision. A risk without a predetermined strategy in place is similar to playing soccer with no “goal posts.” A business leader has a planned outcome in mind before taking action. A businessperson’s leadership skills allow him or her to push, pull and prod others of the necessity of the vision and plan. The above qualities alone will not take your business to success. In addition to risk-taking and leadership skills, you need managerial qualities to power your business. Those are the three traditional defining attributes of the business owner. If you are lacking in any of these three areas, can you still become a broker? Or are you forever destined to be an agent, standing in the shadow of your broker of record? There exist very successful entrepreneurs who break that traditional mold and have learned that by leveraging the skill sets of others in areas where their own skills are not strong, they can acquire the experience, education and drive to achieve success by utilizing a strong workforce that becomes the foundation of their business. Successful and proven franchise models do exactly that. With defined goals that follow a tried-and-true business playbook, coupled with constant testing and improvements to processes, a franchisor provides franchisees with a system that only requires the business owner’s desire to succeed. Franchisors are not only selling their brand names but also their ideas, systems — and, more significantly, their track record. Brokers can focus on revenue generation, the fuel that drives business, instead of testing and adapting a playbook as the market around them changes and evolves. The franchisor has the ability at all times to see the bigger picture providing a valuable back-stop to business decisions that might otherwise cripple a singular business owner. For those who are brave enough to consider opening your own real estate brokerage (my own market area is Ontario, Canada, so I also detail specifics required for Ontario Realtors), you will need to assess the following areas: Business creation and registration One of the hassles that deter real estate brokers from opening their own brokerage is the initial work involved in establishing a corporation and all the paperwork involved. There are a lot of important details when setting up your own real estate brokerage that need to be followed, and often in a specific order. 1. Brokerage application and registration paperwork Filling Real Estate Council of Ontario (RECO) and Toronto Real Estate Board (TREB) forms requires a truly detail-oriented individual. In addition to forms, you have to coordinate other paperwork such as your police background check, transfer forms, bank account setup and signature cards, and so on. You need to be aware of each step of the process and constantly coordinate and follow up with different agencies and individuals. You will need to organize your action plan to get through the initial stages or assign someone who is detail-oriented enough to handle your registration paperwork on your behalf. 2. Incorporation and business registration These two areas will require the services of experienced lawyers and accountants to guide you through the steps. From the choice of business name to the type of corporation your business will adopt, the decisions you make will be need to be coordinated with your brokerage application and registration. You will also need to register and open your Canada Revenue Agency accounts, provincial tax and employer accounts, and other government accounts for filing and reporting compliance. 3. Creating systems and processes In order to operate your brokerage efficiently, you have to put processes in place, even if you are the only registrant or employee in the brokerage. There could be a wide range of processes that you want to establish ranging from office procedures to closing policies. Some of the basic processes to be established are: transaction process, funds disbursement process, trade record sheet process and your recruitment process (if you are recruiting new team members). In addition to systemizing your processes, you might have to work on having an extensive office policy and office culture policy prepared. Planning ahead will save considerable time, effort and headaches when they are needed as your brokerage grows. 4. Searching for office space After crunching your numbers and deciding to open your own brokerage, you have to figure out where you want to locate your office. If you are opening an independent brokerage, you are free as a bird. If you want to be part of one of the established franchise brands, you are restricted as to where you can open your doors. Your franchise brokerage boundaries are more limited in cities, as most territories are already taken in major urban centers. Once the location of your brokerage is determined, you have to start searching for office space within your area. While searching for office space, you have to tackle issues such as type of property, size of space and parking access. The biggest issue about office space that most brokers do not feel comfortable about is the long-term lease commitment. Generally speaking, most office spaces are for a term of five years, which is a significant expense commitment, especially if it is a larger space. In addition, you need at least the first and last month’s rent deposit. Some individuals run their brokerages out of their homes, which I absolutely do not recommend, as it might tarnish your image. You have to ask yourself: Does a home office instill confidence in my ability and success to my clients? I would confidently say that if you are planning to open your brokerage out of your home, you are probably better off staying at your current brokerage. 5. Office furniture and equipment Now that you found your space, you have to start looking for furniture and equipment that fits and matches with your business’s personality. But before moving in the furniture, your office space might need renovation or at least cosmetic touch-up. You have to plan all these steps and, more importantly, reserve time and money to complete them. The cost of renovations and furnishing could easily run up into the tens of thousands of dollars, depending on the size of your office and your interior decorating choices and options. 6. Hiring administrative staff Before your office door opens, you should probably hire someone to answer your phone calls, and you might also need to hire someone else to handle your transactions: a deal secretary. As you can already appreciate, you have to go through the process of interviewing, employee selection and training. You need to first internalize and digest the process of your office yourself, and then transfer it to your staff. This in itself can be daunting for some brokers. This is just the beginning — next week, look for the second installment of the guide to launching your own brokerage. James Hussaini is the founder and president of Realty Point. Email James Hussaini. Read the article in INMAN BY JAMES HUSSAINI March 25, 2015 Every generation lives through, and inspires, change. Although personal values might remain a constant across generations, the tools and information available to help make decisions changes with the times. The mere access to information, generally speaking, does not make people smarter. They need to know which information sources to trust as they wind their way through life. Millennials have lived their whole lives with technology at their fingertips, but does that make them more independent of needing helpful advice and a knowledgeable professional by their side? Certainly not. Does technology replace the important aspects of a real estate agent’s value or does it enhance it? I would suggest that technology enhances the capabilities of a real estate agent’s efforts when used appropriately. And I’d suggest that because of that technology, which is available to all, expectations are higher that the real estate agent’s knowledge is more comprehensive about neighborhoods, local services and the general livability of any particular home in any specific area of the city. In the auto sales industry, the buying cycle has been shortened through consumers’ use of technology to research and select the vehicle of their choice. The car sales cycle 15 years ago was four to eight trips to several dealerships that had the type of vehicle a person was searching for. Now they start online, and when they are ready to make the purchase, they head to the dealership that has their choice in stock, which greatly shortens the sales cycle. The available tools for today’s homebuyers far exceed any basic MLS listing. Those tools require real estate agents to exhibit their knowledge in a variety of channels to make sure potential homebuyers’ search results will yield that real estate agent, which, in turn, will shorten the homebuyers’ sales cycle. It’s very easy to find out everything a homebuyer would want to know about a neighborhood including transit, schools, neighborhood shopping and entertainment venues. Even local crime rates can be found online. Niche and neighborhood expertise is what millennials want to find their real estate agent is capable of — just as any other buyer does. This is no different from home sales of 30 years ago. The real difference is that anyone with basic online search skills can find the information, and millennials are just savvier at finding that information online and deciding if the source is reliable. It’s up to the real estate agent to package the information in a way that provides real value to their client, to understand how to position themselves online to be found and to be the real estate professional who exceeds expectations. Reposted with permission from Realty Point; read the full white paper. What do you do to specialize your service for millennials? Please share in the comments section. James Hussaini is the founder and president of Realty Point. Email James Hussaini Read the article in INMANWhy the traditional brokerage model is obsolete? What Inman's research says about the industry?2/10/2015  BY JAMES HUSSAINI February 10, 2015 Traditionally, a real estate salesperson joined a brokerage for the power of its marketing and name recognition, relying on the “higher power” to drive leads and sales. Changes to the commission split structure put more and more marketing responsibility on the individual. The shift to social media and enhanced online networking systems has dramatically lessened the power of the brokerage over the individual and now provides less and less value to the successful salesperson. 1. Changes that broke the brokerage model. There has been significant shifts in the real estate brokerage industry and none of the changes has been as significant as lower commission splits. Today the commission splits are ranging from as low as 95/5 to a couple of hundred dollars per transaction going to the brokerage. As you might imagine, with such low commission splits, a brokerage can survive only with a very high volume of sales. The margins of gross income and profitability is constantly dropping for the typical real estate brokerage. On one hand, there are not enough resources to properly manage and train the salespeople, and on the other hand the broker of record is constantly looking to generate more revenue to cover his overhead and expenses. Basically, most brokerages are operating “hand to mouth,” and a shock to their business, such as a couple of their top-producing salespeople leaving, can jeopardize their business. With the intention of protecting their business, brokerages are recruiting any licensed salesperson walking into their office. One of the main tools used by brokerages to attract real estate salespeople was and still is the promise to give them leads. The basis of that “promise” ranges from doing “duty time” at the office to online sources. In most brokerages, if not all, this promise is rarely kept. The brokerages cannot keep their promise either due to lack of resources to generate the leads or the number of leads generated is much lower than the number of salespeople. Further, even if brokerages provide leads, they are usually of very low quality, which salespeople consider a waste of their time to pursue. Moreover, the brokerages promise to provide “full coaching” and “hands-on training” for salespeople joining their brokerage. Again, due to a lack of resources, most brokerages cannot afford to provide the training required for their salespeople. As a result, most salespeople are not fully equipped to practice “properly” and “professionally” in the field. Additionally, most salespeople are not compensated for the cost of the technology they do use on a daily basis. With the increase in functionality of smartphones and tablets, the costs associated with the use of technology has shifted from the brokerage to the salesperson. Nowadays, there is another promise used as a recruiting tool to attract salespeople and that is online marketing and branding. It is very challenging to practically carry out this type of promise, as “online branding” is very “personalized.” In today’s age of “content marketing,” each individual salesperson has to be engaged with the online world and create their own individual brand and identity. This may involve writing blogs, posting videos, being active on social media, etc. … Practically, it is almost impossible for a brokerage to brand salespeople individually, as it needs a wide range of resources to accomplish this time-intensive task. So this most recent promise, along with previous ones, cannot be practically delivered even if brokerages had good intentions of carrying through. The lack of supervision, training and coaching has led to another phenomenon in our industry — a significant increase in part-time real estate salespeople. On one hand, these salespeople receive a big commission check, once in a while, which excites them to stay in the real estate industry, while on the other hand they are not confident enough to leave their full-time job for a long-term real estate career. Basically they are not dedicated enough to be fully focused on their real estate career or professional development. As a result, most real estate brokerages have become more of a babysitting and license-stacking office. Real estate salespeople are not fully invested into their career and therefore the rate of making errors or “unprofessional conduct” is high. The broker of record is constantly putting out fires that are created by salespeople, mostly by part-timers. Instead of having a long-term vision to properly train and manage salespeople, brokerages are busy handling issues created by their untrained salespeople. Unfortunately, the real estate brokerage industry has brought this upon themselves by constantly and continuously discounting their services. Conversely, despite receiving higher commission splits, the salespeople feel that they are not getting the level of services they expect from their brokerage, such as training, coaching, and, more importantly, their broker of record being a sounding board and offering support for their transactions. When salespeople do not perform well, they blame their brokerage for their lack of performance. This situation could lead to an environment of lack of confidence in the brokerage. As a result, salespeople are moving from brokerage to brokerage looking for those “promises” to be delivered. 2. Salespeople are the owners of their own “brand.” Salespeople who push forward to establish their own online brand often do not seek out the help of their brokerage other than to see what available tools they have access to. In fact, the traditional real estate brokerage franchise is not in a position to help the salesperson build their own individual online marketing plan, as each salesperson has their own unique characteristics and they can better create their own unique online footprint. In the past, brokerage and franchise branding might have provided some value to the image of individual salesperson, but in today’s online marketing world each individual is better off to create their own brand image independently. For this very reason, most salespeople do not see the value behind the concept of paying the so-called “monthly franchise fee,” and this issue is reflected in Inman’s most recent survey of independent brokers, published on Jan. 5, 2015. Although personal branding has always been the biggest differentiator in the real estate sales industry, now it is the main “primary motivator” for the consumers of today. The expectation of today’s customers is “customized services” that align with their values, lifestyle and specific needs. There is no longer a “one-size-fits-all” strategy that built brokerages in decades past. Each client expects to be treated as an individual. Traditional brokerages and franchises have systemized their processes and provided a “one-size-fits-all” model for their clientele base that is no longer relevant to the expectations of the client. The role of real estate professionals is even more important today than ever before, as clients expect the prompt delivery of customized and personalized services. This trend is clearly demonstrated in a recent survey conducted by Inman. “Brokers and real estate professionals surveyed by Inman say local control of branding and technology gives indie brokers the ability to craft nimble, profitable businesses that can adapt quickly to local market conditions — without the burden of franchise fees.” 3. Consumers pay the price. Our primary mandate as professional salespeople is to protect the interest of our clients. I am not sure how we can serve our clients to the level of service that is expected when we have not received professional training and ongoing coaching. As mentioned earlier, consumers expect “personalized” and “individualized” services when they hire a real estate sales representative. I would like to remind my colleagues that 80 to 90 percent of successful real estate sales professionals’ business is based on repeat clientele and their referrals. You cannot expect to build your business if you don’t have a solid “fully satisfied” clientele base. 4. What is the solution? Our industry is no longer seeing much of any value in the traditional real estate brokerage franchise model, and, as a result, the opening of independent brokerages are the route more brokers are taking. Real estate professionals are rapidly moving toward establishing their own brokerages under their own name and creating their own brand. They prefer not be attached to the “traditional brokerage” image and, more importantly, want to take advantage of incorporating their real estate practice for tax saving strategies and taking charge of their own future. Interestingly enough, “nearly 9 out of 10 Inman readers surveyed (86 percent) think independent brokerages are becoming more popular among real estate agents.” This trend is prevalent in the U.S., which is more or less reflecting our industry here in Ontario as well. Inman points out that “while 71 percent of affiliated brokers surveyed by Inman report that they have thought about going independent, 97 percent of indie brokers say they aren’t considering joining a franchise brand.”  The real estate professionals who investigate the feasibility of opening their own brokerage very soon realize the overwhelming overhead cost and significant amount of time required to handle the administration of the brokerage office. Moreover, additional resources are necessary to meet RECO requirements and be up-to-date with changes in rules and regulations. Generally speaking, most of them are successful as salespeople, and they prefer to be out there selling properties and not stuck in an office to shuffle through papers and accounting reconciliations. Further, we can appreciate that a good salesperson is not necessarily a good administrator, a good bookkeeper or a good manager for that matter. For these very reasons, there are a high number of successful real estate salespeople who do not dare to open their own independent brokerage despite all its advantages. Reposted with permission from Realty Point; read the full white paper. James Hussaini is the founder and president of Realty Point. Read the article in INMAN |

AuthorBelieving education is power and has the ability to generate wealth – Jamshid has made a commitment to sharing his knowledge and expertise in the real estate. Categories

All

|

RSS Feed

RSS Feed

|

|

How we each choose to participate in our social responsibilities, as well as our business dealings, is what will create the world we want to leave for our children...

|

Copyright (c) 2009 - 2022 Hussaini.ca